By Ranga Srinivasan and Ramprasad Satagopan

As financial advisors in Cupertino, CA, Everest strives to provide guidance and education on wealth management matters. We hope this article sheds some light on your questions and concerns.

Giving back to your favorite cause can be a rewarding experience, both emotionally and financially. When ready for charitable giving, you are often faced with choices such as donating from a savings account, stock account, or a retirement account. These options can appear simple at the outset, but they are nuanced in terms of maximizing your giving.

It is not uncommon for a typical donor to face issues including:

- I have appreciated stock; how can I optimize my donation?

- I want to donate regularly each year.

- I want to donate from my IRA, since I am retired.

- I want to make a big long-term commitment.

- I would like to leave money to charity after my time.

The U.S. government encourages charitable giving in the form of tax-breaks, so by planning your giving strategically, your charity can receive more. Let’s explore your options.

What Are My Options?

If you are undecided about specific charities but ready to earmark funds now for a future donation, vehicles like Donor-Advised Funds (DAF) are great choices, since they allow compounding of assets inside the account and increase the giving level, while you enjoy tax advantages at the same time. If you have enjoyed tremendous career success and have accumulated a significant estate, setting up charitable trusts may be important. (1) Charitable trusts, while complex to set up and administer, can be a powerful vehicle that allows you to set up income streams for beneficiaries, potentially defer capital gains tax, or lower your estate tax. (2)

Let’s get into more specific situations.

How Can Qualified Charitable Distributions (QCDs) Help With My IRAs?

If you are over 72, taking Required Minimum Distributions (RMD) from your Individual Retirement Account (IRA), and don’t need the cash flow from distributions to meet living expenses, you have the option to donate some of these distributions to charity (since the IRS has waived ordinary income taxes owed (3) on the distributions as long as they are used for charitable purposes).

This approach allows you to fulfill your RMD obligations while supporting a cause you care about, potentially lowering your tax burden from the RMDs. If you are over 70½, QCDs allow tax-free transfers directly from IRAs to qualified charities. Some benefits include:

- Up to $105,000 per year can be donated tax-free.

- QCDs count toward satisfying RMDs if over 73.

- The donated amount is excluded from taxable income, potentially lowering the donor’s tax bracket.

- May reduce the cost of Medicare premiums by lowering Adjusted Gross Income (AGI).

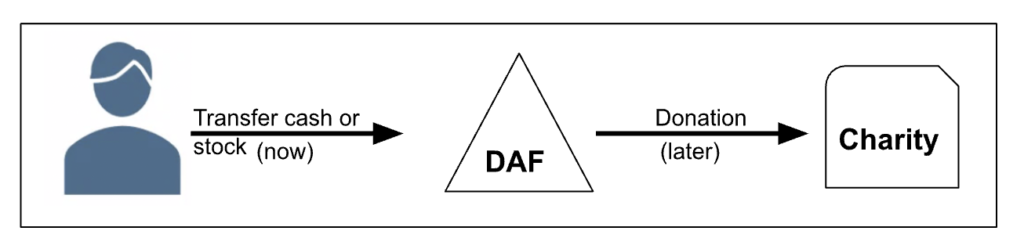

How Can I Give Appreciated Stock Using a Donor-Advised Fund?

Are you ready to create and fund an investment account earmarked for future charitable donations? A DAF could be the perfect choice since it facilitates charitable giving by allowing contribution of investment assets to a fund, receiving an immediate tax deduction, and then recommending grants to charities over time.

Contributions made to charities through a DAF account instead of writing checks from your investment account has some advantages:

Funding the DAF Account: Appreciated securities (in the form of stocks or mutual funds) can be moved to a DAF account, and thus avoid capital gains taxes on the appreciation, while taking an immediate tax deduction as long as it does not exceed a certain percentage (4) of AGI for the calendar year.

Investment Growth: Inside the DAF account, assets can be invested for tax-free growth, potentially increasing the amount available for charitable giving.

Flexibility and Control: Donors can recommend grants to any eligible IRS-approved 501(c)(3) public charity at their own pace. DAFs also simplify the process of charitable giving by consolidating multiple donations into a single account, providing one tax receipt, and allowing for strategic, long-term philanthropic planning.

Accessibility: DAFs are accessible to a wide range of donors, not just the ultra-wealthy, and can accept a variety of asset types, including complex assets like private stock and real estate.

Can I Do Some Estate Planning With IRAs and DAFs?

Designating your favorite charity as a beneficiary of your IRA can also be a strategic estate planning move, as it can potentially reduce income and estate taxes for heirs and help your legacy support future needs of charity. You can avoid including unused IRAs in estate tax calculations and potentially avoid double taxation (5) on inherited IRAs.

You can also name your DAF as a beneficiary of your IRA for posthumous giving—so your charity can benefit from your generosity even after your lifetime.

How Do Charitable Trusts Help Me Make a Big Long-Term Commitment?

Setting up charitable trusts (6) can be important depending on your charitable goals and financial situation. Two Trusts that are popular are the Charitable Remainder Unit Trust (CRUT) and Charitable Lead Annuity Trust (CLAT). CRUTs and CLATs are typically used (7) by ultra-high-net-worth donors who have charitable intentions and at the same time interested in tax deferral of capital gains, income streams to beneficiaries, potentially some ordinary income tax deduction, or removal of assets out of their estate. Let’s discuss the specifics of these two trusts.

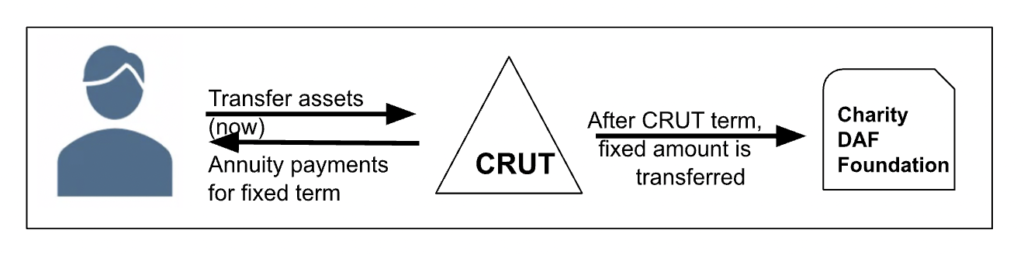

CRUTs

A CRUT is an irrevocable trust set up for a fixed term (10, 20, or 30 years), during which non-charitable beneficiaries receive income streams. After this period, the remaining assets in the trust are transferred to a designated charity.

Key features include:

- Income Stream: Beneficiaries receive a steady income for life or a set term, which can be beneficial for retirement planning or providing for family members.

- Tax Benefits: Donors can potentially avoid capital gains taxes on appreciated assets placed in the trust and receive an immediate charitable income tax deduction based on the Present Value (PV) of the remainder interest that will eventually go to charity.

- Types: There are two main types of CRTs: Charitable Remainder Annuity Trusts (CRATs), which pay a fixed annuity, and Charitable Remainder Unitrusts (CRUTs), which pay a fixed percentage of the trust’s value, recalculated annually.

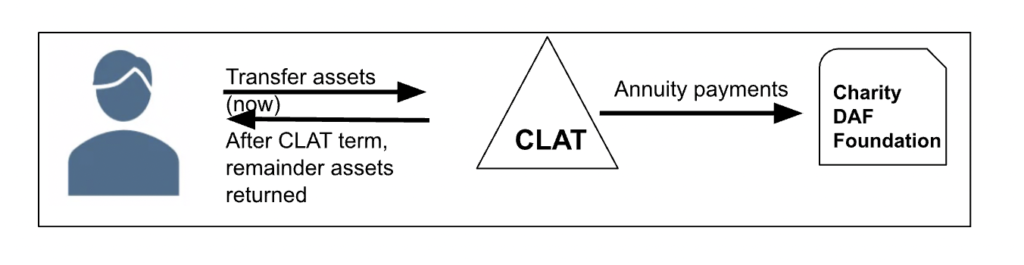

CLATs

A CLAT reverses the sequence of recipients as compared to CRUT: charities get income streams for a fixed period of years (anywhere from 10 to 30), and at the end, the remainder of assets get passed on to beneficiaries.

Key features include:

- Immediate Charitable Impact: The charity receives regular payments during the trust term, making it ideal for those who want to support a charity in the short term.

- Tax Benefits: CLATs can offer potentially significant gift and estate tax benefits. The donor can take a charitable gift tax deduction for the present value of the annuity payments to the charity. The remainder assets that get transferred to beneficiaries are potentially excluded from estate tax calculations of the donor (grantor).

- Flexibility: The remaining assets after the term can revert to the donor or be passed on to heirs, potentially reducing estate taxes.

How Do I Choose Between a CRUT and CLAT?

The decision between a CRUT and a CLAT depends on your financial goals and charitable intentions:

- Income Needs: If you need a steady income stream now or in retirement, a CRUT might be more beneficial.

- Immediate Charitable Support: If you prefer to support a charity immediately and potentially reduce estate taxes, a CLAT could be the better choice.

- Tax Considerations: Both trusts offer potential tax benefits but of different kinds, as the specifics can vary. It is highly recommended to consult a tax advisor before making the choice. CRUTs in general can offer potential income tax benefits and capital gains tax deferral, while CLATs can be advantageous for gift and estate tax planning.

We’re Here to Help

By exploring these charitable giving options, donors can make a meaningful impact on their charity’s future while optimizing their tax savings. Please consult your financial advisor, tax professional, and estate attorney to get guidance on maximizing your giving.

Everest Management Corp, a wealth management firm based in Cupertino, CA, is here to help you navigate your options. We employ a fiduciary wealth management model, which means our financial planners prioritize clients’ interests above all else. If you’d like to learn more, we invite you to schedule an introductory, no-obligation meeting by contacting us at 408-502-6015 or emc@everest-mgmt.com.

About Ranga

Ranga Srinivasan is co-founder and principal at Everest Management Corp, an SEC-registered wealth advisory firm based in Silicon Valley and serving clients across the United States. After graduating from the University of Cincinnati in the field of engineering, Ranga, witnessed the dot-com collapse in the early 2000s and sought to manage his own personal finances. He realized that many of the options available were unsatisfactory for a myriad of reasons. Knowing it could be done better, Everest was founded in 2007 to provide comprehensive wealth management. Ranga and the Everest team are dedicated to caring for the financial needs of the families they serve. With an emphasis on building trust and holding to the fiduciary standard of putting clients first, Ranga strives to offer financial solutions that inspire confidence.

In his free time, Ranga is passionate about staying active; you can often find him swimming, golfing, biking, and playing tennis. He also has a great love for charity and philanthropy work. To learn more about Ranga, connect with him on LinkedIn.

About Ramprasad

Ramprasad Satagopan is co-founder and principal at Everest Management Corp, an SEC-registered wealth advisory firm based in Silicon Valley and serving clients across the United States. As a self-made, highly educated first-generation immigrant, Ramprasad became passionate about investing after witnessing the dot-com collapse in the early 2000s. He created Everest to help his peer engineering community to build household wealth in a systematic way. Everest has grown over the years while staying true to its fiduciary commitment. Ramprasad and the Everest team take pride in being a firm that brings a reputable, honest, and caring approach to all its clients.

Ramprasad graduated from both the University of Cincinnati and the University of Phoenix with a master’s degree in science and business administration, respectively. When he’s not helping families build a strong financial future, Ramprasad can be found enjoying traveling and reading. To learn more about Ramprasad, connect with him on LinkedIn.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These views may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Investing in REITs involves certain distinct risks in addition to those risks associated with investing in the real estate industry in general. Equity REITs may be affected by changes in the value of the underlying property owned by the REITs, while mortgage REITs may be affected by the quality of credit extended. REITs are subject to heavy cash flow dependency, default by borrowers and self-liquidation. REITs, especially mortgage REITs, are also subject to interest rate risk (i.e., as interest rates rise, the value of the REIT may decline).

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Everest Management Corp. strategies are disclosed in the publicly available Form ADV Part 2A.

Everest Management Corp. is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Everest Management Corp. and its representatives are properly licensed or exempt from licensure.

_________________

(1) Setting up charitable trusts should not be initiated without expert consultation from a team of estate attorney, tax advisor, and financial advisor.

(2) Illustrations and references for tax reduction are not to be construed as tax advice. Please consult with a tax professional with regards to your specific situation.

(3) Illustrations and references for tax-reduction are not to be construed as tax advice. Please consult with a tax professional with regards to your specific situation.

(4) IRS allows tax deduction for up to 30% of AGI for donation for non-cash contributions, and 60% of AGI for cash contributions. Please consult with your CPA for specifics.

(5) Illustrations and references for tax-reduction are not to be construed as tax advice. Please consult with a tax professional with regards to your specific situation.

(6) Setting up charitable trusts should not be initiated without expert consultation from a team of estate attorney, tax advisor, and financial advisor.

(7) Some of the typical use cases are described here. For specific recommendations, please consult with your estate attorney, financial advisor, and tax planner.